- Real Estate Navigator

- Posts

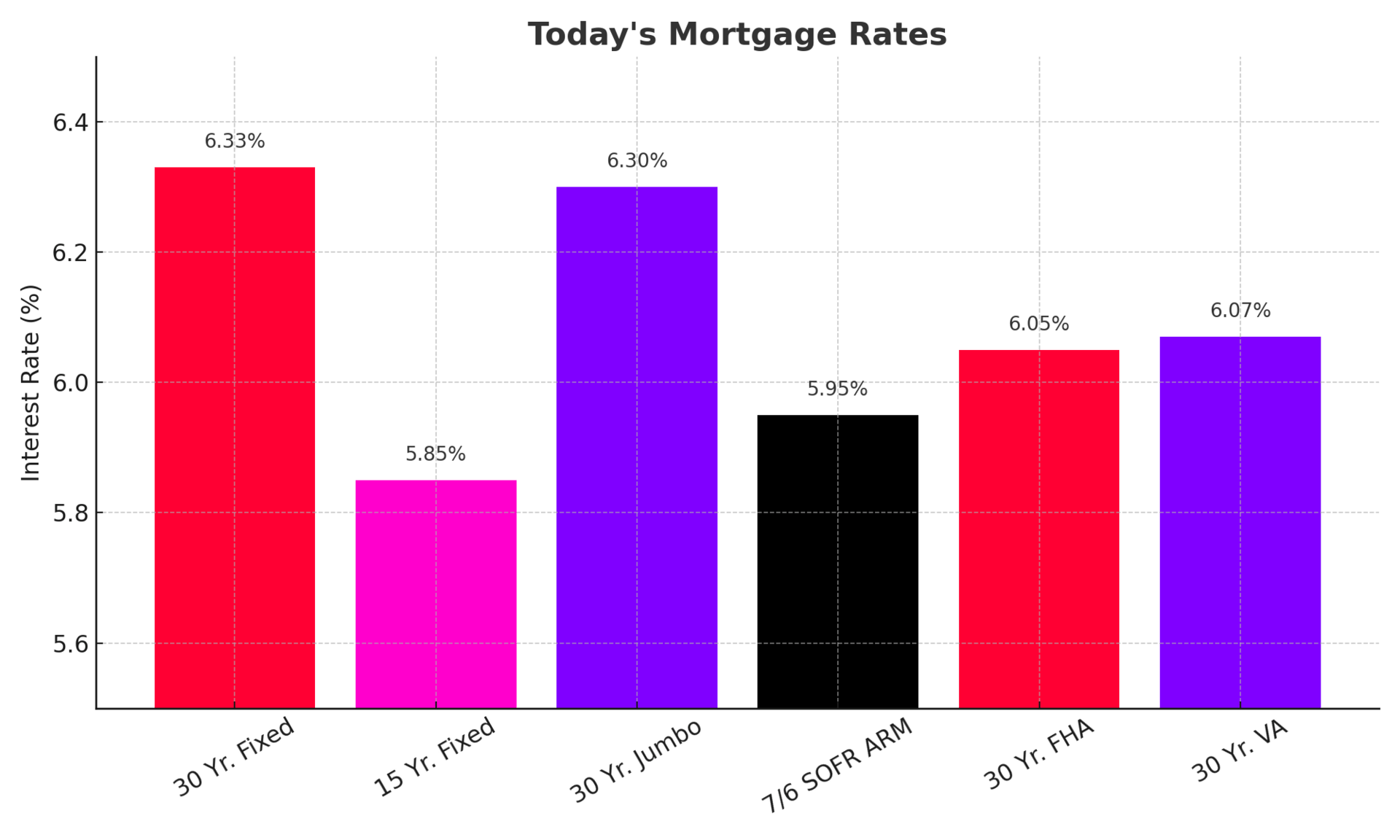

- Mortgage Rates 101: Why They Don’t Move With the Fed

Mortgage Rates 101: Why They Don’t Move With the Fed

Understanding the real levers behind rising and falling rates

Real Estate Navigator

October 31, 2025

Why Mortgage Rates Don’t Always Follow the Fed

You’ve probably heard it: “The Fed just cut rates, so mortgage rates will drop too.”

Except…not always. Mortgage rates and the Federal Reserve move in the same orbit, but they’re not attached at the hip. Let’s break down how the system actually works.

The Fed Funds Rate: The Short-Term Player

The Federal Funds Rate is what banks charge each other for overnight loans. It’s a short-term rate that influences things like credit cards, car loans, and savings yields.

Mortgage rates, on the other hand, are long-term loans, think 15 or 30 years. They move based on what investors expect the economy and inflation to do over that entire stretch of time, not just this month.

Think of it as:

The Fed Funds Rate = short sprint.

Mortgage rates = marathon.

Meet the Real Influencer: The 10-Year Treasury Yield

If you want a sneak peek at where mortgage rates are heading, skip the Fed meeting livestream and check the 10-year Treasury yield instead. That’s the bond investors use as a benchmark for mortgage-backed securities—the bundles of home loans traded on Wall Street.

When the 10-year Treasury yield rises, mortgage rates usually climb too. When it falls, mortgage rates often follow.

Why? Because investors want to earn a little more on mortgages than they do on Treasuries. The spread between them is where your home loan rate lives.

Inflation, Economic Data, and Market Expectations

Here’s the twist: even if the Fed cuts rates, mortgage rates can rise if investors think inflation is heating up again or the economy is running strong.

Every week reports on jobs, consumer spending, and inflation shift the outlook. If markets believe inflation will stay sticky, long-term yields go up—and mortgage rates go with them.

So, a Fed rate cut doesn’t guarantee cheaper mortgages. It just signals that short-term borrowing is cheaper. The bond market decides the rest.

Why Everyone Gets Confused

It’s not your fault. The Fed does affect mortgage rates indirectly—through its tone, forecasts, and inflation fight, but there’s no one-to-one relationship.

When the Fed raises rates to cool inflation, long-term rates sometimes drop if investors believe the plan will work.

When the Fed cuts rates to spur growth, long-term rates can rise if investors fear inflation will rebound.

Translation: what matters most is what the market believes will happen next, not what the Fed does today.

What This Means for Buyers and Sellers

For Buyers:

Don’t wait for “the next Fed cut” to trigger a magical mortgage drop.

Watch the 10-year Treasury yield instead, it’s a better crystal ball.

If you find a good home and a fair rate, consider locking it. You can always refinance later if rates fall.

For Sellers:

Buyers’ affordability depends on rates, but market sentiment shifts fast.

A small drop in Treasury yields can re-energize demand overnight.

Stay flexible on timing, today’s “slow” market could wake up quickly if inflation cools.

Bottom Line:

The Fed sets the tone, but the bond market sets the price. Mortgage rates dance to the tune of inflation, investor expectations, and long-term confidence in the economy, not just the Fed’s headlines. For buyers and sellers, that means focus less on Fed chatter and more on the bigger picture: affordability, timing, and strategy.

Until next week!